[Property Address]

The property located at [Property Address] is officially in foreclosure as of [Date FC Filed] according to [Clerks Office]. If no further action is taken, a foreclosure/sheriff’s sale will be ordered by the courts and the property will be sold at auction.

There’s no shame if you find yourself in foreclosure. Homeowners have options to avoid a foreclosure/sheriff’s sale and to save a home from foreclosure. There are rights protection homeowners in the state of Florida.

WHAT DO I DO NOW?

Don't Panic!

- Recognize that a foreclosure is a legal problem.

- Know that as a defendant; you have certain legal rights.

- Consult an Attorney:

- When you are served with a Complaint –A legal action has begun against you.

- All legal matters require timely responses.

- Not taking action worsens the situation.

- An attorney will be able to advise you on how best to resolve the matter.

- Even if you have not taken timely action, an attorney may still be able to help.

- Do not write a letter to the court as you will waive your affirmative defenses if your letter does not address each allegation

FORECLOSURE STEPS

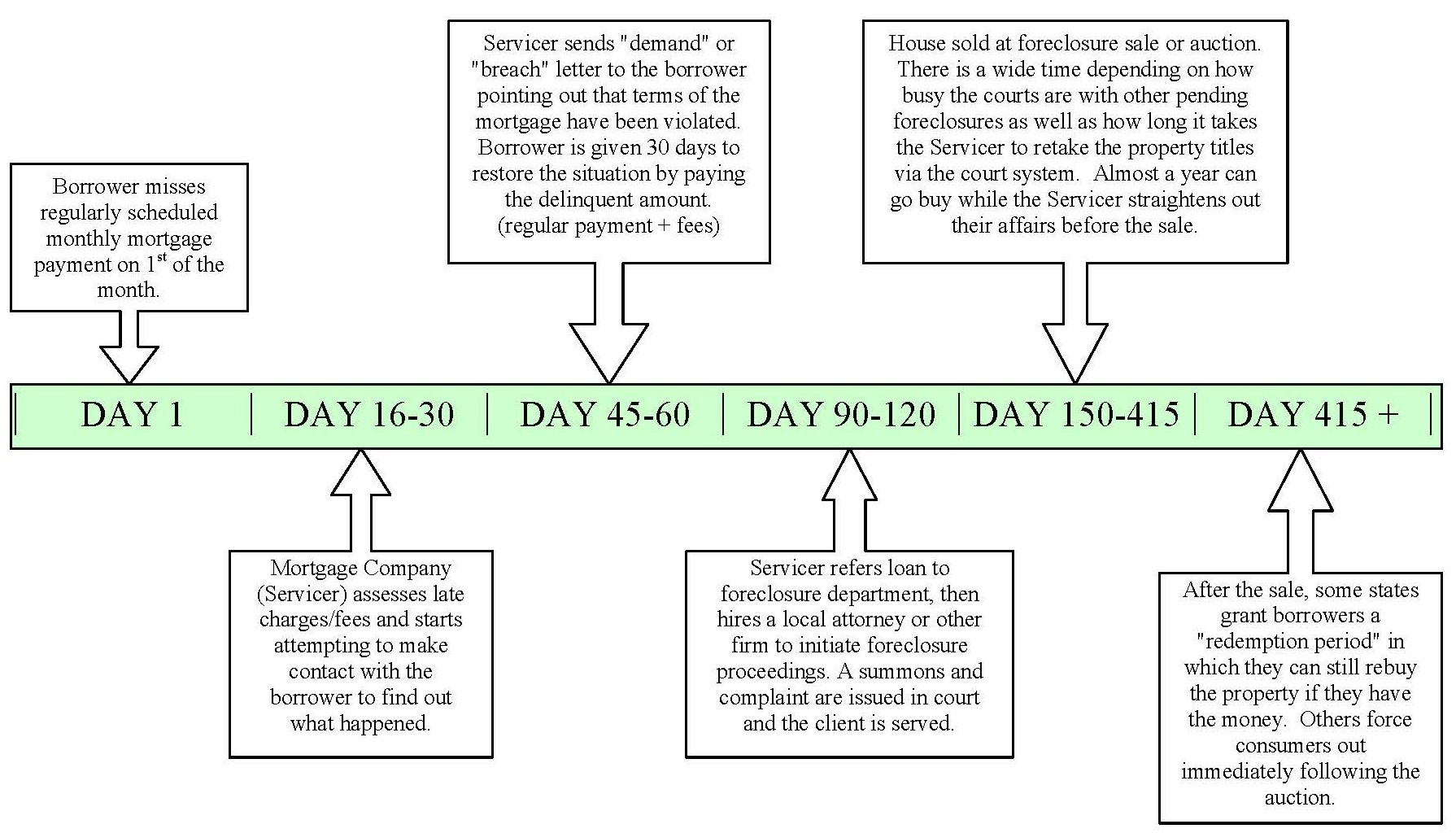

Step 1:

After a homeowner is between 45 to 90 days behind on their mortgage payments, the mortgage servicer will send the homeowner a “breach” or “demand” letter stating that they are in default and need to take action to resolve their delinquency. Typically a 30 time period is given to cure the delinquency by either bringing the loan up to date or paying off the loan per the Acceleration clause.

Step 2:

If a homeowner is unable to cure the loan in 30 days, the the lender/servicer will file a “complaint.” The “complaint” is a lawsuit against the owner to foreclose on the home. The homeowner will be served with a summons and complaint by a sheriff or process server and have only 20 days to respond. If they do not respond, the the lender will likely receive a default judgment. If they do respond, the foreclosure case will go to either a summary judgment or trial.

Step 3:

The lender will likely try to make a motion for summary judgment first, meaning the material facts of the case are not in dispute and the lender will receive a final judgment of foreclosure against the homeowner. If the material facts surrounding the case can be reasonably disputed, then the case may proceed to trial.

Step 4:

At a foreclosure trial, the homeowner’s attorney and the lender/servicer will present their evidence to a judge who will make a decision regarding the case. If the judge hands down a final summary judgment (final judgment of foreclosure), the foreclosure will move forward and a foreclosure/sheriff’s sale date will be set to auction the home.

Step 5:

The sale of the home must be publicized for at least two weeks, and then the actual sale will occur. At the foreclosure auction/sale, the home will be sold to the highest bidder. Whether the highest bidder is a third party or the lender/servicer the home will be sold.

Step 6:

Assuming the lender/servicer purchases the home (very typical); the lender will then seek a certificate of title from the Clerk of Court. Once they obtain the certificate of title, they will officially possess the home. At that time they can file a Writ of Possession to have the previous homeowner evicted from their now former home.

Step 7:

A sheriff will come by and serve the Writ of Possession to the homeowner and they will have 24 hours to vacate the premises or be removed by the sheriff.

FORECLOSURE TIME LINE

WHAT ARE MY OPTIONS?

Keeping the home:

- Hire an experienced attorney to defend foreclosure

- Have an attorney start working on a “work out” plan with your lender

- Special Forbearance Plan

- Repayment Plan

- Loan Modification

Not Keeping the home:

- Pre-Foreclosure Sale

- Deed-In-Lieu of Foreclosure

- Bankruptcy

WHERE CAN I GET HELP?

- [NEED TO DISCUSS WHAT CALL TO ACTIONS TO ADD HERE]